Looking Back And Looking Forward In The Cattle Industry

DR. ANDREW P. GRIFFITH

KNOXVILLE, TENN.

In this article one year ago, there was a discussion about college football, cattle prices and how a crystal ball would be helpful in figuring out both subjects. However, even a crystal ball would have had difficulty predicting this past year. College football has moved from the BCS era where the top two teams in the rankings vie for national bragging rights to a system with a four team playoff to determine the national champions. Is this change an improvement? That question is yet to be answered, and there is sure to be more grumblings until every team is included in the playoff and everyone wins a trophy! Similarly, cattle prices the past year moved from a level considered to be strong to a new level that was unimaginable to most in the industry. Is this change an improvement? The short answer is ‘it depends.’

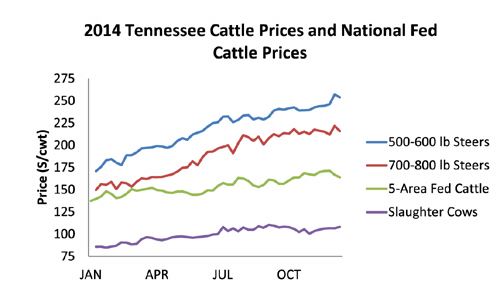

Fed cattle prices started out 2014 trading over $137 per hundredweight on a live basis and steadily increased throughout the year peaking in November at $171 before losing some ground in December. Similarly, the Choice boxed beef price started 2014 at the $200 per hundredweight mark and then escalated to its peak near $262 in August before losing a little ground in the fall.

A little closer to home, 500 to 600 pound steers started 2014 trading about $171 per hundredweight based on weekly auction market averages. They seemed to push higher all year before topping out just above $257 in December. The story is not much different for 700 to 800 pound steers which started the year just under $150 per hundredweight and escalated to $218 in October.

So, is this change in price levels an improvement? There is one sector that has benefited tremendously and that is the cow-calf sector. There is little to no negative effects from the price escalation on cow-calf producers in the near term. However, producers’ management and marketing decisions through these record high calf and feeder cattle prices could have major implications when the market flips and prices start to decline.

Stocker producers and backgrounding operators benefited greatly from the steady increase in prices throughout the year. The steady increase in prices generally allowed producers to purchase cattle on a low market relative to the market they were selling on which resulted in record margins on many cattle. However, prices started flattening in the fall time period which returned margins to more normal levels. This can be viewed as problematic because producers have been investing 50 to 60 percent more money into cattle than in previous years and the margins are the same. Thus, financial risk in these operations has escalated and there is no ideal way to manage the increased risk.

A similar situation is evident in the feedlot industry. However, they will soon start feeling the squeeze from the output price side as packers are starting to find it difficult to push wholesale beef prices higher. Pushing wholesale beef prices higher will be a constant challenge the next several years as consumers eye the retail price of beef relative to the retail price of pork and poultry products.

Outlook: The year 2014 will go down in the record books as the year cattle prices exploded to record highs? It is very doubtful cattle prices in 2015 will be able to maintain the trajectory witnessed in 2014. Low cattle inventory and retention of heifers to rebuild the cattle herd will continue to support market prices, but increasing retail prices for beef and pushback from the export market will limit the ability to push prices higher. The average 2015 price for all classes of cattle is expected to exceed the 2014 average. Much of that increase in average prices will be due to how low prices were in the first half of 2014 relative to the second half of the year.

In 2015, cattle producers may witness small increases in calf and feeder cattle prices relative to a year ago but a more seasonal trend to prices is expected to reenter the market. Cow-calf producers should continue to benefit from elevated prices while margin operators will have to manage margins carefully to turn suitable profits. Just like there will be a number of teams in college football who go home without a trophy this year, not everyone in the cattle industry is going to win a trophy in 2015. ∆

DR. ANDREW GRIFFITH: Assistant Professor/Department of Agricultural and Resource Economics, University of Tennessee