Something new will happen on 23 November 2020 in the world rice market. CMEGroup will launch a cash-settled Thai white rice 5% broken FOB futures contract, based on Platts assessment. This is the first rice forward product with some promise of success since US rough rice futures moved its operations to Chicago in 1983. I discuss the journey for that contract below. I identify why this rice futures may succeed where so many others have failed. At the end of this essay, I review the success factors that led to a market in US rough rice, as a guide to this new initiative.

In this analysis, I draw upon my 40 years in the rice futures business, as a major commercial rice buyer and hedger from 1981-1999 for Mars Incorporated and since 2000 as a rice market risk advisor and economic analyst for Firstgrain.

I think this Thai contract just may make it. All new businesses that succeed are somewhat of a miracle, where events and participants conspire to make it happen, hence, the quote above from Emerson, who was fascinated with the realm of miracles. Over the last 30 years I have watched the US futures contract grow agonizingly slowly. Meanwhile, I have seen rice futures ideas come and fail in London, Bangkok, China and India. There are two small domestic and very high-priced rice markets in China and Japan.

For a few months in Dalian, China, back in 1996, a milled rice futures market started up and became the largest traded grain market contract in the world at that time. Several months later the government shut it down just because it became too successful.

The special role of rice in Asia

Based on many years of visiting Asia, I see two commodities Asian investors love or would love to trade: yellow gold and white rice. Rice is their life food. Governments have been reluctant to let the public trade a futures market in the price of their cash rice for many reasons. Unlike the US, Asia has experienced many famines and seen their children die of starvation. The US has known only two major periods of famine: The War of 1812 and the Civil War. The US is a blessed nation with unparalleled, natural resources.

Our company, Firstgrain, derives its name from a Chinese proverb, “More precious than pearls or jade are the five grains of which rice is first.” What does this mean? If means simply that if your children are starving, you will sell the family jewels to buy them rice. This comes home to us all during this global pandemic. Life gets down to whether your child will have a school lunch today, even in the US. Who would have thought this would happen in 2020?

Some contract specifications

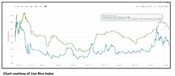

Below is a chart of the Thai 5% market versus the US 2/4% milled rice market prices over the last 8 years. As you can see, there are periods with wide price disparities and in general rice prices in the Americas trade at higher levels than rice prices in Asia. A lot more work needs to be done to show the relationships, if any, between Asian rice origins in the Far East and rice export markets in the West.

For further information on the New Thailand White Rice 5% (Platts) futures contract, please check out: The new Thailand Long Grain White Rice (Platts) futures contract

Here is the announcement for the new CME Group contract:

“CME Group offers cash-settled Thailand Long Grain White Rice futures to complement our existing suite of physically delivered US Rough Rice futures and options. The Thailand Long Grain White Rice (Platts) futures contract tracks closely to its respective cash market for 5% broken rice and allows firms to manage price exposure to Thailand and other competing white rice exports.

The contract is based on the Platts daily price assessments for Thailand Long Grain White Rice 5% Broken, FOB stowed and trimmed one safe berth, load port Bangkok, on conventional vessel, for shipment 15-45 days ahead.”

Basic Advantages of new contract:

• Effective price risk management tool for Thailand, and other competing origins, long grain white rice export markets

• Cash-settled basis – the Platts Thailand Long Grain White Rice assessment (no physical delivery)

• 12 calendar months, available for trading

• Daily price settlements provided by CME Group for 12 calendar months

• Available to trade electronically and as privately-negotiated blocks through an active broker market on CME ClearPort

• Spreading opportunities with CBOT US Rough Rice futures

What is the contract and when will it be launched?

The Chicago Board of Trade (CBOT) Exchange of CME Group is launching a Thailand Long Grain White Rice 5% Broken FOB Financially Settled (Platts) Futures contract (pending CFTC review). The contract size is 25 metric tonnes and quoted in US$ and cents per tonne. The commodity code is TRF. The first trade date is 23 November 2020 and 2021 will be the first contract month available for trading and clearing.

Who will oversee the contract?

The new Thailand White Rice (Platts) futures contract is listed in the U.S. by CBOT and cleared in the US by CME Clearing. The regulator is the CFTC.

What are the contract specifications?

The price assessment reflects the export price for Thai origin Long Grain White Rice classified as 5% broken. This refers to the maximum content of broken rice in the cargo. Platts LRI will normalise to the 5% broken standard for contracts, bids or offers that vary from the stated quality.

The price assessment reflects the following characteristics:

• Origin and Quality: Thailand Long Grain White Rice, 5% broken

• Cargo size: 1,000-5000 metric tonnes +/- sellers’ option. Delivery Location: FOB Bangkok

• Loading period: 15-45 days ahead of the assessment day.

What is the settlement price of the contract?

The final settlement price for each contract month is equal to the arithmetic average of the “Thailand Long Grain White Rice 5% broken FOB” price assessment published by Platts for each day that it is determined during the contract month, rounded to the nearest $0.01.

What are the position limits?

The Thailand White Rice Financially Settled (Platts) Futures will have a Spot Month Limit of 2,500 contracts for all calendar months. Single Month Accountability Level and All Month Accountability Level are both set at 2,500 contracts.

What is the listing schedule?

Monthly contracts will be listed for 12 consecutive months of the Thailand White Rice Financially Settled (Platts) Futures contract. A new monthly contract will be added following the termination of trading in the front month contract.

What price is used to settle the contract value?

Any remaining open positions after the last trading day of the contract calendar month are cash-settled rather than physically delivered. Cash-settlement is based on the Final Settlement Price of the contract month, which is equal to the arithmetic average of the “Thailand Long Grain White Rice 5% broken FOB” price assessments published by Platts during the contract month.

This venture comes on the back of a successful launch three years ago of Black Sea corn and wheat contracts. These two contracts trade more volume than the US rough rice futures contract. Like the Thai White Rice 5% futures contract, the Black Sea grain contract is settled in cash, not physical delivery. This should give early traders of the contract the assurance they can get out of the position at delivery. In addition, delivery is priced FOB vessel in Bangkok harbor. Also, financially the contract trading and settlement is cleared in the US by CME Clearing, guaranteeing performance of the contract, and removing counterparty risk.

At my previous employer I owned about half of the contract open interest on the New Orleans exchange at times and when it was shut down Jun 15, 1983 in New Orleans, I was in a not so comfortable position as a commercial hedger.

Unlike previous launches, the CME Group Thai Rice futures contract will settle off Platts daily posted price for Thai White Rice 5%. If the industry does not like price discovery, they should get used to it, as it has already happened with Platts. In addition, Thailand is healing from a bad rice policy implemented back in 2011-2014 that built up huge stocks to manipulate the market price. More recently, the market has suffered from severe drought which has reduced export activity. It is recovering from bad rice policy followed by a drought.

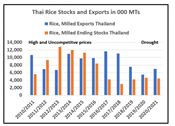

You can clearly see in the above bar chart that from 2010-2016 Thai rice stocks built up dramatically and trade dropped off from 2011-2013. This is a classic case of very bad rice policy for a rice exporter. Although stocks are back to a manageable level since 2017, the drought in 2019-2020 has taken its toll, again reducing exports.

My point here is that Thailand has come through very hard times and now may be coming out the other side.

Asia Rice: A Brief History Lesson

For 1000 years, Thailand has traded and exported commodities, more recently rice. We wish them well in the years ahead. Thailand has not suffered the plague of famine and starvation to the degree of other Asian countries. Most famines are induced more by humans than by Mother Nature anyway and can be solved by allowing rice to trade freely.

In addition to this cash-settled Thai white rice futures contract, Platt’s LRI has started up a forward curve in the Thai 5% market, which might complement the new futures initiative.

Thailand has a history of open markets stretching back at least to 1292 AD.

I conclude with a quote. Much of what is known about this glorious time of growth and invention comes from a stone inscription scribed by the Thai King in 1292:

“There are fish in the water and rice in the fields. The ruler does not levy a tax on the people who travel along the road together, leading their oxen on the way to trade and riding their horses on the way to sell. Whoever wants to trade in elephants, so trades. Whoever wants to trade in horses, so trades. Whoever wants to trade in silver and gold, so trades" Henceforth Sukhothai was regarded as the "golden age" of Thai history, literally "the dawn of happiness".

Notice rice was not specifically mentioned in the above ancient quote.

The US rough rice contract has gone through important modifications over the last 17 years. As changes were made, the basis (the cash minus the futures price) after 2012 stabilizes at a more reasonable range of values over time. Expect that the new Thai White Rice 5% contract may need changes to enhance volume and price liquidity. All futures contracts are a “work in progress.”

The wide swings in open interest and volume are related to market conditions as well as flaws in the contract design. The Thai White Rice 5% futures has the opportunity to become a much larger market than US rough rice futures. Most rice trades as a milled product on the world market.

Think back to 1986 when the CBOT launched the rice futures contract on the big grain floor. It had made a checkered journey from New Orleans to the MidAm floor in Chicago. The New Orleans Commodity Exchange or NOCE was an underfinanced exchange for rice and cotton. Actually, rice futures first failed in New York City during the 1960s as a milled contract to hedge PL480 business. The milled rice contract was restarted in New Orleans in 1981 and a rough rice contract was also launched for the farmers to use at that time. Both contracts crashed by 1983 and moved to Chicago. Only the rough rice contract survived the move from New Orleans to Chicago. The US has yet to launch a milled rice contract that works.

Looking back on the journey, rough rice futures required the following developments. Rough futures benefited from some important changes and chances in the marketplace since 1985:

• Congress approved the Rice Marketing Loan in 1985. Without this new policy rough rice futures would have died under the weight of large rice stocks and a loan support well above the price in Thailand and other Asian origins.

• Slowly with the help of river barges to Latin America, volume and market size picked up.

• We have also had several changes to the delivery instrument and the contract design implemented to help the contract grow.

• Some large companies were committed to making it work on the buy and the sell side of the market from the outset. I worked as rice buyer and hedger for one of these companies, Mars Incorporated.

• Arkansas firms participated and were familiar with the process of setting and trading the basis of cash to futures. Arkansas had such grain merchants, familiar with hedging corn, wheat, soybeans, and cotton. In addition, Don White, my good friend, and his company, White Commercial, helped teach local merchants how to merchandise rice effectively using rice futures. Education and the opportunity to manage risk is at the core of all successful ventures in futures start-ups.

• Launching a futures contract is similar to launching a small business. It needs firms with a “can do” attitude that see opportunity in change. Forward thinking businesses see change as a miracle and opportunity.

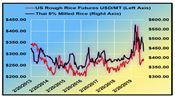

Is there an arbitrage opportunity between US long grain rice futures price and Thailand Long Grain White Rice 5% Broken FOB Financially Settled (Platts) Futures contract ? Perhaps, there is or will be. Almost 25% of US domestic demand for milled rice comes from aromatic imports of Jasmine from Thailand and Basmati from India. So, the US and this part of Asia rice production are commercially joined at the hip. The volatility of US and Asian 5% rice prices have picked up dramatically in 2020. The red line in the chart below is Chicago long grain rough rice futures. The black line is the Thai 5% cash price.

The two markets, Thai milled rice and US rough rice, do relate to each other; but the arbitrage between them will most likely increase as the Thai White Rice 5% milled rice (Platts) futures becomes more of a standard for pricing of exported rice in Asia. Most rice traded globally is in milled rice, not rough rice, with the exception of the US market for domestic mills and export to Latin American destinations. The trade in rough or paddy rice is largely prohibited by the large rice exporting nations of Asia.

We stand at the dawn of a potentially new era for rice trading, or “the dawn of happiness”. To quote a contemporary of Mr. Emerson, Henry David Thoreau, “All change is a miracle to contemplate; but it is a miracle which is taking place every instant.” Picture rice trading on-line and digital and taking place every instant across time zones and the oceans of the world. It could happen. I think it will happen. ∆

For information concerning The Rice Market Strategist, please contact Milo Hamilton at milo@firstgrain.com (Office Telephone: 512 345 0497) Cell Phone 512 658 8761